DENVER — As younger generations welcome pets into their lives at an increasing rate, the pet food landscape is beginning to shift toward fresher, minimally processed formats enhanced with health and wellness claims, according to a recent report from CoBank. Though dry, standard “brown-and-round” pet foods still make up the bulk of the pet food market, fresh, refrigerated and frozen formats are witnessing significant growth as younger consumers begin to dominate pet ownership.

According to CoBank’s “Seeking Wellness, Younger Pet ‘Parents’ Spur Pet Food Growth Trends” report, dollar sales of fresh dog and cat foods have increased 86% and 54%, respectively, in 2021. Volume sales for this segment have outperformed the entire pet food category, with unit sales of fresh dog food rising 47% and those for fresh cat food increasing 20% during the past two years.

Additionally, health and wellness attributes, like weight management, healthy aging and calmness, are making an impact with younger pet parents, providing brands further opportunities to attract these consumers with such claims.

“Today’s pet owners are treating their pets as well as, or better than, themselves,” said Billy Roberts, senior food and beverage economist for CoBank. “As human health trends increasingly inform pet nutrition innovations, new ways to support pets’ overall wellbeing will continue to emerge, whether in the form of foods, treats or supplements for their pets' physical and behavioral health.”

The current landscape

As shared by the American Pet Products Association’s (APPA) 2023-2024 National Pet Owners Survey, 86.9 million US households (about two-thirds) own at least one pet, with ownership among Millennials and Gen Zers equaling that of Gen Xers and Baby Boomers. Additionally, according to APPA’s “State of the Industry: Strategic Insights from the National Pet Owners Survey 2024” report, ownership among Gen Zers is the only cohort to have witnessed growth from 2018 to 2024, increasing from about 10% to 16%, whereas ownership among other generations have remained flat or even decreased.

Though these younger pet owners are focusing on more premium, minimally processed diets that carry health benefits, they currently spend less on pet nutrition products compared to older pet owners. According to MarketWatch, Gen Xers spend the most annually on their pets’ food at an average of $949, accounting for 0.81% of their income, followed by Baby Boomers who spend an average of $842 annually, but spend the largest percentage of their income compared to other generations at 1.07%. Millennials spend an average of $679 annually, accounting for 0.74% of their income. Gen Zers spend the least, an average of $369 annually, though their spend represents the second-highest percentage of their income compared to other generations at 0.83%.

CoBank expects that as Gen Zers age, grow into their careers and expand their income levels, their overall spending should increase throughout the food and beverage space, including in the pet food and treat industry.

The pet food and treat industry has continued to benefit from evolving pet ownership and consumer demand, but worsening inflation has plagued the industry. Though inflation is a problem experienced by almost every other industry, including food and beverage, it is particularly significant for the pet food industry. According to CoBank, pet food inflation has consistently outpaced national inflation since December 2021. This rising inflation has caused many pet parents to trade down in their pet food purchases. According to research from Mintel, four in 10 pet parents would consider switching to a lower-priced pet food alternative amidst continued price increases, demonstrating opportunities for smaller brands and private labels to expand their market share.

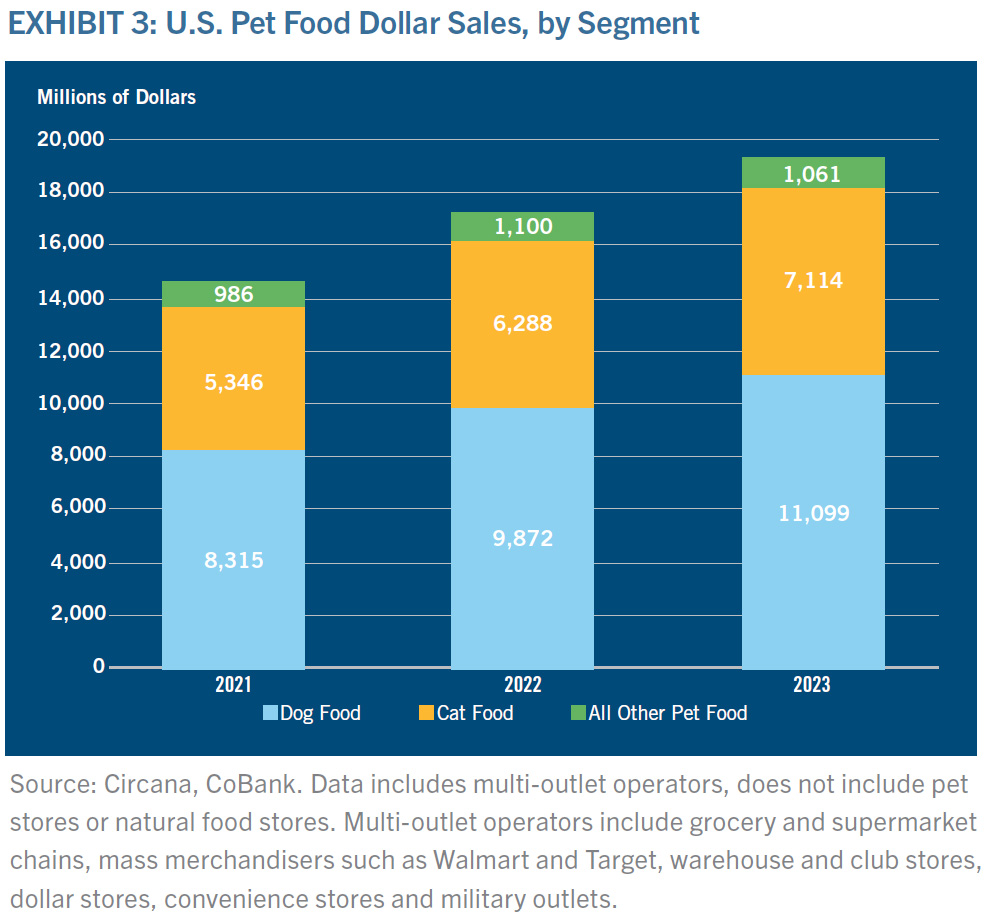

According to CoBank, dollar sales for the US pet food market hovered around $19.3 billion in 2023, an increase of 11.7% from 2022. However, this increase in sales is largely attributed to rising prices, as sales volume decreased 2.5% in 2023 compared to 2022. According to data from Circana, dollar sales for the pet food industry have risen nearly 32% since 2021, with dog and cat food witnessing growth of over 33% each.

Source: Circana, CoBank

Source: Circana, CoBank

Overall, sales volume across all pet foods have dropped over the past couple years. According to CoBank, dog food volume dropped 5.2% in 2023, with the bulk of this decline occurring in wet dog food, a more preimmunized segment. However, cat food sales volume mostly kept pace with its 2022 numbers, dropping a mere 0.4% in 2023.

All about fresh

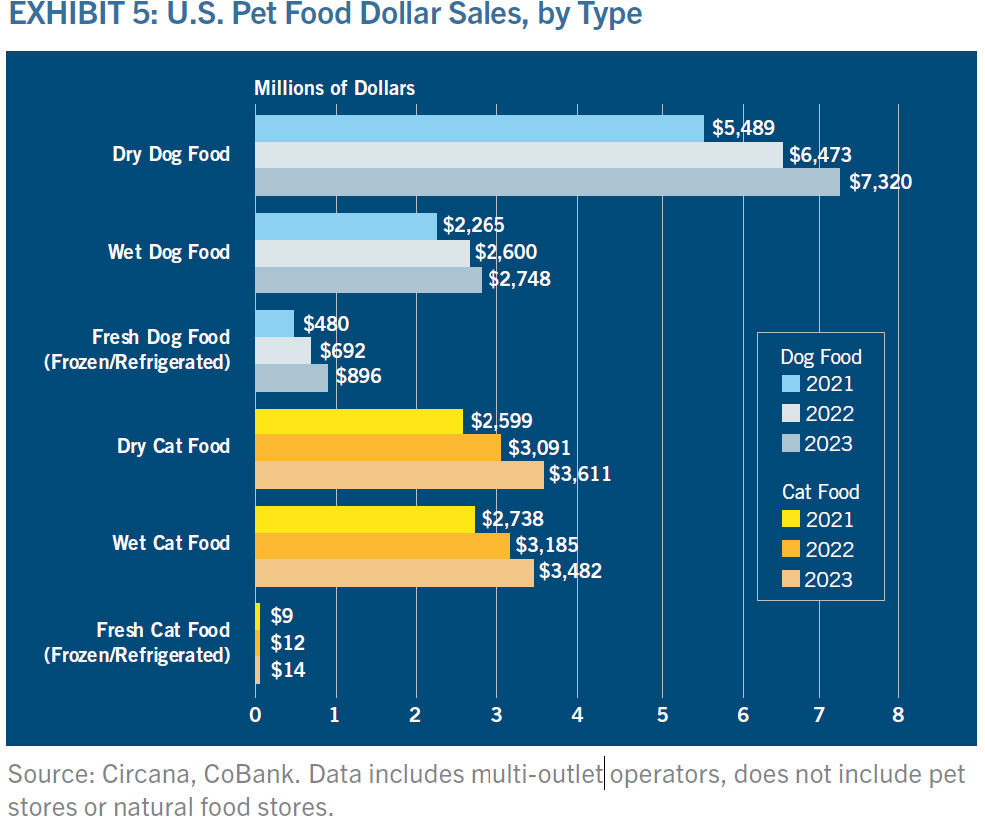

Though dry pet food accounts for the largest market share in the industry for both dog and cat foods, fresh formats, like those bagged dry or even canned or pouched wet, are experiencing more rapid growth.

According to CoBank, since 2021, fresh/frozen dog food dollar sales have risen 86.5% and those for fresh cat foods have risen 53.8%. In 2023, sales volume also rose for both segments at 19.2% for fresh dog food and 6.4% for fresh cat food. This significant increase in volume is also seen over the past two years with fresh dog food increasing a whopping 47.2% and fresh cat food increasing 19.7%. Additionally, CoBank found that fresh dog food accounted for about 4.6% of total dog food dollar sales in 2023, an increase from 3.3% in 2021.

“Consumers generally equate fresh options, particularly refrigerated products, with foods that are natural and, by further extension, healthier, and such leaps of logic likely continue to fuel growth in the foods people are buying for their pets,” Roberts wrote in CoBank’s report.

Source: Circana, CoBank

Source: Circana, CoBank

Freshpet is currently the major player in the fresh space, though the company’s capacity constraints are likely to provide opportunities for other smaller players seeking to gain share, according to Roberts. Additionally, Bloomberg anticipates that the fresh, refrigerated/frozen category will account for 11% of the pet food market by 2030.

Mintel’s research adds on to this, with the company finding that 51% of US pet food purchasers perceive freshly prepared foods to be healthy, and nearly 79% are willing to pay more for health pet nutrition products.

Optimizing wellness

The growing trend in fresh pet foods also speaks to the humanization trend, which has caused an influx of products boasting functional benefits from oral health to weight management to life-stage specific benefits. In fact, Mintel’s Global New Products Database found that 21% of new pet food products launched in 2023 included a vitamin or mineral fortified claim, and 40% featured a low or no or reduced allergen claim. Humanization and function are also penetrating the pet treat category, as consumers continue to seek pet treat products that mirror their own dietary demands and are free from perceived “unhealthy” ingredients.

As awareness of pet health spreads, the word “health” has also evolved for pet parents. Therefore, the nutritional solutions have shifted, targeting almost every possible aspect of pet health from the gut microbiome to behavior.

Weight has become synonymous with pet health, with the Association for Pet Obesity Prevention (APOP) raising awareness on the “pet obesity epidemic.” According to the association, more than half of all dogs and cats were classified as overweight or obese in 2018, and this has only continued to rise. In APOP’s “2022 State of US Pet Obesity” report, the association revealed that 59% of dogs and 61% of cats were classified as overweight or obese.

To help “trim the fat” so to speak, pet parents have sought out weight management or weight loss pet foods to help bring their pets back to optimal body condition and health, fueling an influx of pet nutrition products that address weight from processors. Younger pet owners are more aware of this epidemic, according to CoBank, as 41% of consumers aged 16 to 34 believe their pet would benefit from some weight loss.

Functional ingredients have permeated the pet food industry as ways to target and optimize pet health, and Roberts expects that such ingredients and wellness claims will continue to evolve.

Pets > kids

In addition to health and wellness trends propelling the pet food industry, Roberts shared that a cultural aspect is at play: declining birth rates. According to data from the United Nations and APPA, shared by CoBank, the US birth rate has dropped from 15.65 in 1988 to 12.02 in 2023, whereas pet ownership has risen from 56% of US households in 1988 to 66% in 2023. Younger generations are delaying — or completely halting — having children, causing many to dedicate their parental instincts toward their pets.

Humanization is also playing a factor here, as puppy- and kitten-specific nutritional products have entered the sphere, homing in on cognitive development, bone health and growth that are seen in infant and toddler foods. Roberts anticipates this trend to continue, claiming that humanization “may have only just begun,” especially as the human-animal bond transforms to become more similar to that between parent and child.

What the future holds

Roberts expects pet food growth will be fueled by the above trends and as inflation eventually abates. Pet owners will look for foods that support elderly or life-stage pet needs and laser in on formulas with quality ingredients, regardless of high price points.

Such attributes are also expected to build upon humanization, with an increasing number of foods and treats made with alternative or non-animal-based proteins to avoid pet sensitivities/allergies or to appease environmentally conscious pet parents.

Other product trends include high-fiber, inclusion of pre-, pro- and postbiotics, and formulas promoting healthy weight, relaxation, immune function, skin and coat health, digestive health and oral health. These products may also come in combination with a trend toward indulgence as owners seek to treat pets with hyper-humanized products, like dog ice cream.

Keep up with the latest pet food trends on our Trends page.