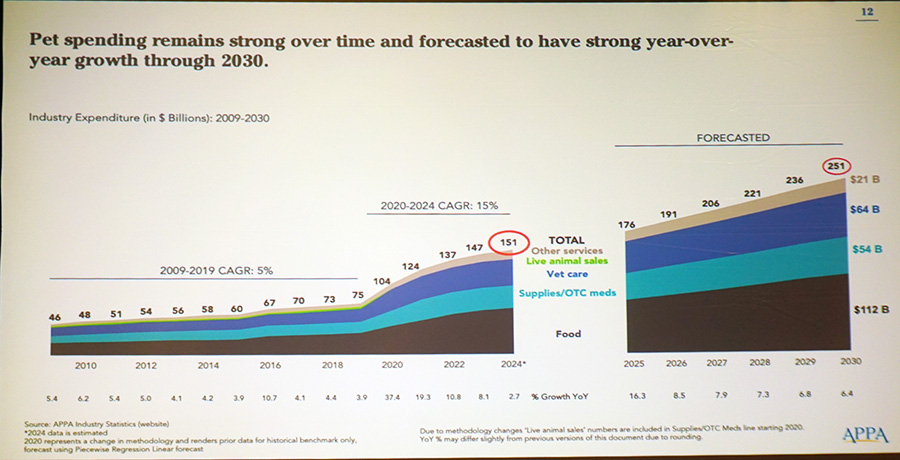

STAMFORD, CONN. — Though pet ownership has normalized to pre-pandemic levels, the US pet industry has continued to reap significant rewards, earning it another strong year of performance. According to the American Pet Products Association (APPA), total industry sales topped $147 billion in 2023, an increase of about $10.2 billion (7.45%) from 2022. The association presented its latest State of the Industry Report during Global Pet Expo last month in Orlando, Fla, anticipating continued growth for all sectors of the pet product industry.

According to the report, the pet food and treat sector remains top dog in terms of sales, totaling $64.4 billion in 2023 and accounting for about 43% of total pet industry sales. This represented an increase of 10.8% from 2022.

Vet care and products sales was the second-highest category, totaling $38.3 billion in sales, up 6.7% from 2022, and accounting for about 26.1% of total industry sales. This was followed by supplies, live animals and OTC medicine with $32 billion in sales, up 1.6% from 2022 and accounting for 21.8% of total industry sales.

The lowest spend category was “other services,” which includes boarding, grooming, insurance, and pet training, sitting and walking, totaling $12.3 billion in sales, up 7.9% from 2022 but accounting for a mere 8.4% of total industry sales.

Additionally, according to APPA, the pet industry supplied an overall economic contribution of $303 billion, an increase of 16% from 2022.

APPA expects the industry’s growth to continue, with sales anticipated to top $250 billion by 2030. Of this, the pet food and treat category is set to achieve around $112 billion in sales. The vet care and products sales category is anticipated to reach $64 billion, followed by supplies and OTC medicine at $54 billion, and other services at $21 billion, by 2030.

“The data has shown that the pet industry has remained incredibly strong since 2009 despite wide-scale economic challenges,” said Peter Scott, president and chief executive officer of APPA. “While there are signs of slowing, the industry is resilient, especially compared to other industries. In fact, we forecast the industry's expenditures to top $250 billion by 2030.”

Chart by the American Pet Products Association, Image by Sosland Publishing Co. / Nicole Kerwin

Chart by the American Pet Products Association, Image by Sosland Publishing Co. / Nicole Kerwin

Pet ownership

In conjunction with this data, APPA also released its State of the Industry: Strategic Insights from the National Pet Owners Survey 2024, detailing slowdowns in pet ownership levels.

According to the report, 63% of US households own a pet in 2024. Of these pet-owning households, 44% own dogs, an increase from 39% in 2010, and 30% own cats, a decrease from 33% in 2010.

The APPA anticipates that pet ownership will reach 67% of US households in 2030. Of this, the association forecasts that 46% will own dogs and 35% will own cats.

The percentage of multi-pet households is also normalizing to pre-pandemic levels, according to APPA. In 2024, about 63% of pet-owning households owned at least two pets, a decrease from 66% in 2022, but flat from 2018.

Generationally, Millennials still account for the largest cohort of pet owners, owning more pets than any other generation, but Gen Z numbers are quickly rising, according to APPA. In 2024, 32% of Millennials owned a pet, steady from 2018. Twenty-seven percent of Gen Xers owned a pet, a slight decrease from about 26.5% in 2018. And 24% of Baby Boomers reported owning a pet, a decrease from about 27.5% in 2018.

Gen Zers remain the smallest cohort of pet parents with 16% owning a pet, an increase from about 10% in 2018, making this generation the only one experiencing growth in ownership.

“Millennial pet owners still account for more pet owners than any other generation, but the number of Gen Z pet owners is quickly rising,” said Ingrid Chu, vice president of insights and research at APPA, during her presentation at Global Pet Expo.

Shopping habits

Though pet parents span from varying generational demographics and tend to spend in different ways, brick-and-mortar remains the most popular way to purchase pet products. According to APPA’s report, 39% of pet owners report purchasing pet products in-person at a brick-and-mortar store in 2024. However, online shopping is close behind with 34% of pet owners reporting purchasing pet products online and having them shipped to their homes, and 7% purchasing online and having them shipped to the store.

Some pet parents prefer to leverage both shopping methods in an omnichannel approach. In fact, 11% report browsing for pet products online but then purchasing them at a brick-and-mortar store, and 7% report browsing in-store but then purchasing online from a different retailer.

The most common pet products purchased online in 2024 have been pet food (79% of pet parents), treats (76%) and toys (69%). Other popular pet products purchased online include grooming supplies (61% of pet parents), litter or bedding (55%) and medication (51%).

The amount these consumers have spent on their pets continues to fluctuate, however many have reported spending the same or less on their pets. For 2024, 30% of pet parents claimed they spent more on their pets, down from 39% in 2022; fifty-one percent spent the same, an increase from 46% in 2022; and 19% spent less, an increase from 15% in 2022.

Breaking down purchasing habits generationally, younger pet owners typically shop for pet products online, whereas their older counterparts typically shop in brick-and-mortar stores. In 2024, 50% of Gen Z pet owners, 52% of Millennials, 46% of Gen Xers, and 42% of Baby Boomers reported purchasing pet products online. On the other hand, 46% of Gen Z pet parents, 44% of Millennials, 51% of Gen Xers, and 55% of Baby Boomers typically purchase in-store.

According to APPA, Gen Zers were the only generation to increase their online purchases of pet products over the past year from 36% in 2023 to 51% in 2024. All other generations decreased their online pet product purchases. Millennials dropped from 48% in 2023 to 42% in 2024, Gen Xers witnessed a decrease from 58% to 32%, and Baby Boomers experienced a drastic decrease from 65% to 24%.

Additionally, COVID caused many pet owners to leverage the power of subscription-based purchasing, a convenient “set-it-and-forget-it” purchasing method for these consumers that has gained staying power. In 2024, 46% of pet parents reported using subscriptions when ordering pet products, an increase from 39% in 2018. Twenty-seven percent reported using subscriptions to purchase pet food, up from 25% in 2018, 15% use subscriptions for pet treats, down from 18% in 2018, and 12% used this purchasing method for pet vitamins and supplements, down from 18% in 2020.

Breaking subscriptions down generationally, Gen Zers are the most likely to have a subscription for their online pet product purchases, followed by Millennials and Gen X. In 2024, 61% of Gen Zers, 51% of Millennials, 42% of Gen Xers, and 35% of Baby Boomers used subscriptions to purchase pet products. For Gen Z pet parents, 33% used subscriptions for pet food, 22% for treats, and 19% for vitamins/supplements. For Millennials, 30% used subscriptions for pet food, 18% for treats, and 14% for vitamins/supplements.

Leveraging resources

Generationally, shopping habits mimic the methods that pet owners utilize to gain more information about their pets and pet products, with younger generations preferring to use online platforms over in-person experts and vice-versa for older generations. However, vets still remain a key resource.

According to APPA’s report, 54% of Gen Z dog owners and 60% of cat owners usually obtained information about their pets via the internet, social media or some other online resource. Forty-five percent of Millennial dog owners and 54% of cat owners obtained information from the same sources. But only 42% of Gen X dog owners and 47% of cat owners, and 39% of Baby Boomer dog owners and 42% of cat owners, used the internet, social media or other online resource to receive more information about their pets.

On the flip side, 48% of Gen X dog owners and 46% of cat owners usually obtained information about their pets from their veterinarian. Sixty-two percent of Baby Boomer dog owners and 50% of cat owners used the same source. But only 46% of Gen Z dog owners and 37% cat owners, and 44% of Millennial dog owners and 39% of cat owners, obtained information from the same source.

In learning about new pet products, younger generations mostly use social media or the internet, whereas older generations become aware of products in-store. For Gen Z pet parents learning about new products, 55% use social media, 48% look in-store, 43% use the internet, and 36% become aware of new products via their friends. For Millennials, 51% become aware of new products in-store, 49% use social media, 48% use the internet, and 39% learn about new products from their friends.

For Gen X pet owners, 54% become aware of new products in-store, 44% use the internet, 39% learn from their friends, and 35% use social media. For Baby Boomers, 57% learn about new products in-store, 36% use the internet, 36% become aware of new products from TV ads, and 36% hear about them from their friends.

When looking to the internet to learn about new pet products, Gen Zers rely on TikTok (56%), YouTube (47%) and Instagram (44%). Millennials use search engines (56%), Facebook (43%) and YouTube (43%). Gen Xers use search engines (62%), Facebook (42%) and pet product websites (42%). Baby Boomers used search engines (62%), pet product websites (50%) and Facebook (35%).

“While brick-and-mortar is still a big driver of awareness of new pet products, social media is equally important among the younger generations,” Chu said. “Gen Z looks to visual platforms like TikTok, YouTube and Instagram to learn about new pet products, telling us that pet brands will need to consider more visual media to reach their younger audiences.”

As pet ownership levels continue to slow for Millennials, Gen Xers and Baby Boomers and skyrocket for those in Gen Z, the pet industry will need to evolve in order to capture these newer, younger pet parents.

Keep up with the latest pet food trends on our Trends page.