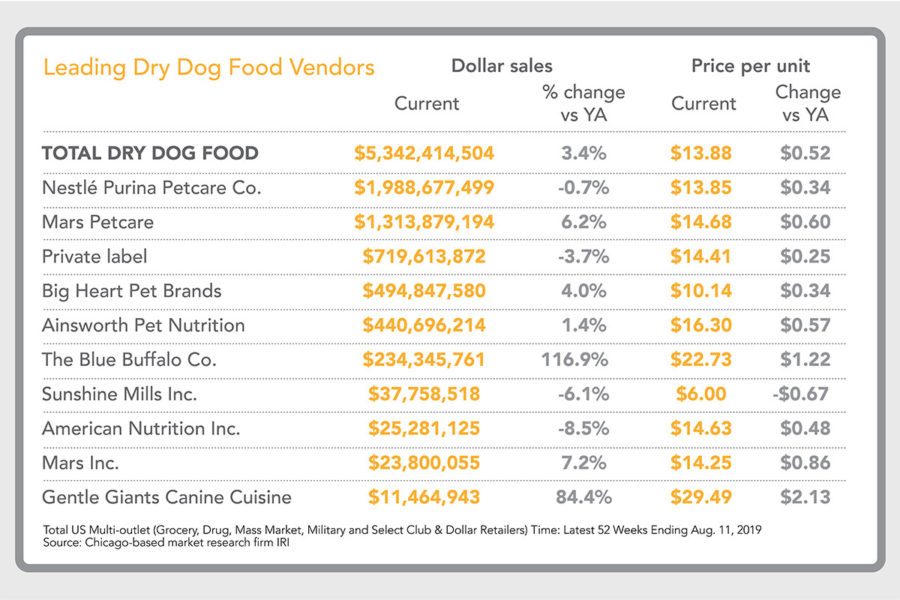

In the big picture, the US pet food and treat industry continued to grow in 2019. That growth has garnered the attention of investors and some large human food manufacturing companies. Both General Mills with the acquisition of Blue Buffalo and J.M. Smucker Company with the acquisitions of Big Heart Pet Brands and Ainsworth Pet Nutrition are now embracing food and treats for pets as key business pillars delivering the growth required by their investors.

Pet food and treat brands are chasing consumer preferences of matching their own personal food philosophies with what they feed their pets, and brands are throwing tradition out the window and distributing to any and all channels in order to meet pet owners where they prefer to shop.

Additionally, the regulatory environment over the past 10 years has brought US pet food processing standards in line with human food manufacturing, increasing the pressure for pet food manufacturers to check and check again that their products can be made safely, consistently and efficiently.

All in all, global human food companies and investors holding more stake in the pet food market, an emerging omnichannel landscape, consumer-driven ingredient and formulation trends and regulatory challenges have proven that with growth comes growing pains, and pet food and treat brands are having to fine-tune their processes and products more than ever to stay competitive.

Changing channels

With Blue Buffalo leading the pack, pet food and treat brands have strayed from their traditional sales channels — either pet specialty, Food, Drug and Mass (FDM), or internet retailers — to unapologetically meet customers where they shop.

“We’re focused on significantly expanding Blue’s availability so that pet parents can get the Blue products they want anywhere they shop for pet food,” said Billy Bishop, Blue Buffalo’s founder and brand adviser, during General Mill Inc.’s Sept. 18 earnings call covering the first quarter of its fiscal 2020 year. Minneapolis-based General Mills acquired Blue Buffalo in 2018.

So far, this approach seems to be working for the super-premium brand. Blue Buffalo sales topped $368 million for the first quarter of fiscal 2020 and were up 7% from year-ago sales. General Mills said retail sales for FDM customers who have carried Blue Buffalo for more than 12 months were up 50% versus last year. E-commerce sales for the pet food brand were up more than 20% in the first quarter as well, according to the company, which expects e-commerce growth to continue at 8% to 10% throughout fiscal 2020.

Unfortunately, as the company shifts focus toward FDM, Blue Buffalo sales in the pet specialty channel declined at a double-digit rate. To repair relationships with pet specialty customers, General Mills has launched a new super premium line, Carnivora, which will be sold exclusively in the pet specialty retail space. As brands are widening their product lines to offer exclusivity to certain channels, those channels are creating brands of their own.

High-end house brands

Until recently, independent pet specialty stores traditionally carried higher priced brands and the lower priced options were available in mass retail outlets. Those lines have begun to blur in the pet food and treat market. Traditional barriers are fading away and premium claims, such as high protein, grain-free and all-natural diets, continue to drive sales.

An increasingly wide variety of premium pet foods have become available through various mass and e-commerce channels, speeding up the “mass premiumization” of the market, according to Packaged Facts’ annual report, “Pet Food in the U.S., 14th Edition.”

House brands have dominated the low end of the pet food market for years, even in pet specialty stores, but this was before premium and super-premium products took over FDM retailer shelves, said Steve Mills, senior vice-president, customer brands and co-manufacturing at American Nutrition Inc.

House brands have dominated the low end of the pet food market for years, even in pet specialty stores, but this was before premium and super-premium products took over FDM retailer shelves, said Steve Mills, senior vice-president, customer brands and co-manufacturing at American Nutrition Inc.

“Now that more premium and super-premium products are migrating from pet specialty to FDM shelves, it creates the opportunity for FDM retailers to create similar brand offerings of their own,” Mills said. These new house brand pet foods have become top-shelf competitors and are attracting consumers with premium ingredients, functional claims and lower price points than top premium brands.

Jared Koerten, an analyst covering packaged foods for Euromonitor International, said millennials who favor both premium and value are helping drive this trend. Private label products are rising in the ranks in pet care, with retailers launching their own brands across all channels and categories. According to the Private Label Manufacturers Association, New York, store brands’ market penetration set all-time records in 2018, increasing dollar share and unit share at double-digit rates.

Novel proteins

Good-for-the-planet brand claims seem to dominate the sustainability story of pet food, and novel proteins are nothing to bark at. Last October, Wild Earth, Inc., Berkeley, Calif., launched a dog treat line made with cultured koji (Aspergillus oryzae), an ancient Asian protein and member of the fungi kingdom containing all 10 amino acids essential for dogs. Then, in August 2019, the company launched a meatless complete-and-balanced diet for dogs that utilizes yeast protein as a main ingredient and source of protein.

In March 2019, Because Animals, Philadelphia, announced the development of pet treats containing lab-cultured meat – a meat-alternative protein made from mice cells. The company, which already offers probiotic supplements for cats and dogs, released its first human-grade dog treat made with nutritional yeast in December 2019 and said it plans to debut a cultured mouse meat cat treat in early 2021.

Jiminy’s, a Berkeley, Calif.-based pet treat manufacturer using crickets as a sustainable source of protein, launched two complete-and-balanced insect-protein dog foods. Good Grub includes insect protein powder, while Cricket Crave includes cricket protein powder. Montreal-based dog food company Wilder Harrier offers an insect protein-based pet diet as well. Most of the diet’s protein comes from the inclusion of black soldier fly powder and oil, which is supplied from Canadian insect-rearing facilities.

As the market is introduced to the promise of new ingredients for pet diets, whether they are derived from yeast, lab-grown meats or insects, the pet food and treat industry is sticking to one important tradition: growth.

History of growth

For more than 10 years, the industry has delivered growth that keeps investors’ tails wagging. The American Pet Products Association (APPA), based in Stamford, Conn., said pet food has grown year over year since 2007 by at least 3.7% and as much as 10.7%.

While dollar sales for dog food continue to trump cat food sales, food for felines has grown and is projected by Packaged Facts to continue growing at a higher rate than dog food. In 2020, cat food sales are projected to grow 3.2% to $9.6 billion, while dog food sales are expected to grow 2.5% but still lead the pack with $19.2 billion. According to Euromonitor, the growth in global cat treat sales led the pack with a compound annual growth rate (CAGR) of 9% between 2013 and 2018, followed by dog treats with a 5% CAGR during the same period.

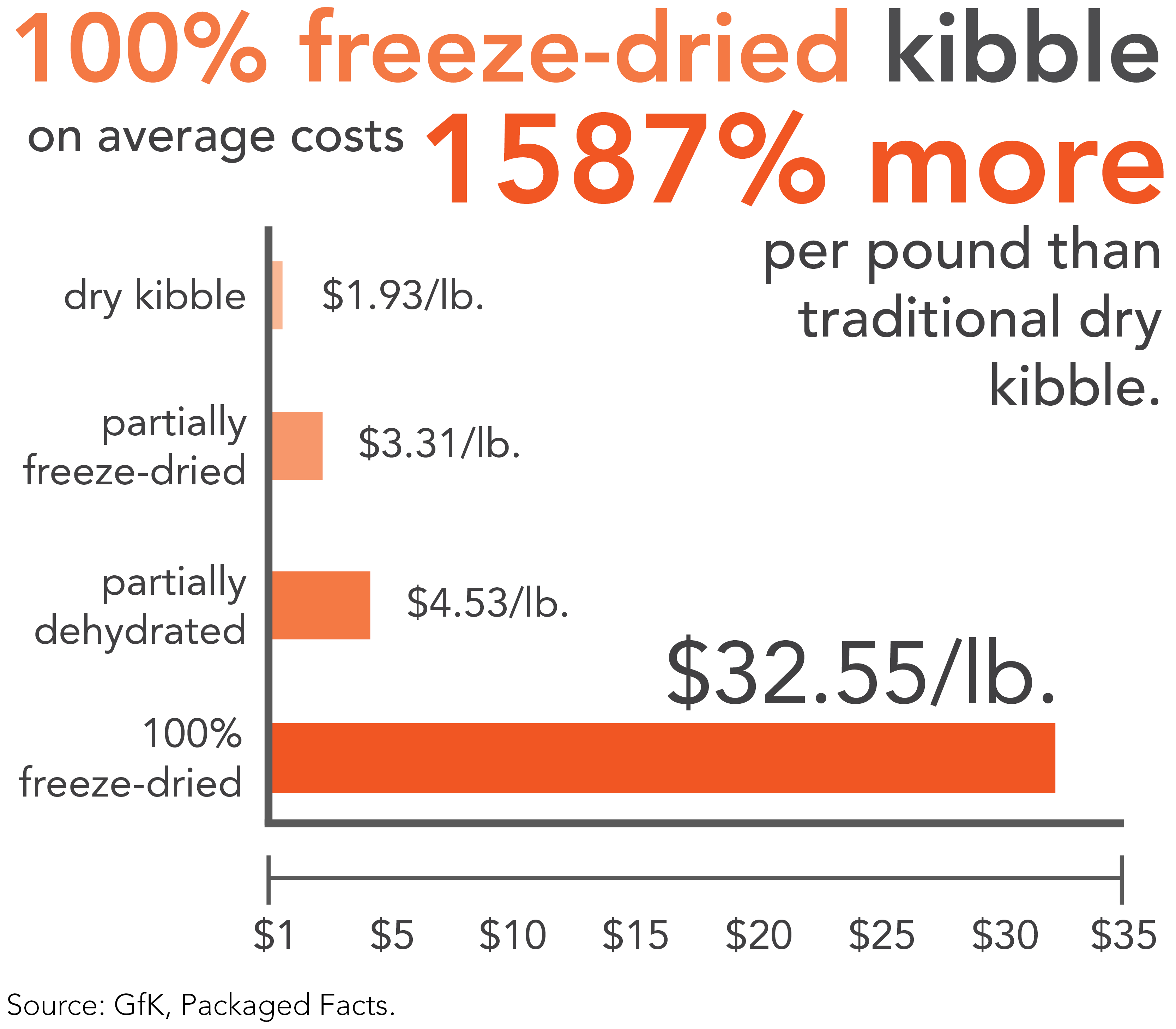

Many new pet food formats, such as dehydrated or freeze-dried, are fetching premium prices, making them an attractive brand extension option. A 100% freeze-dried kibble recipe on average costs 1,587% more per pound than traditional dry kibble, according to Packaged Facts, with 100% freeze-dried costing an average of $32.55 per lb. and dry kibble averaging $1.93 per lb.

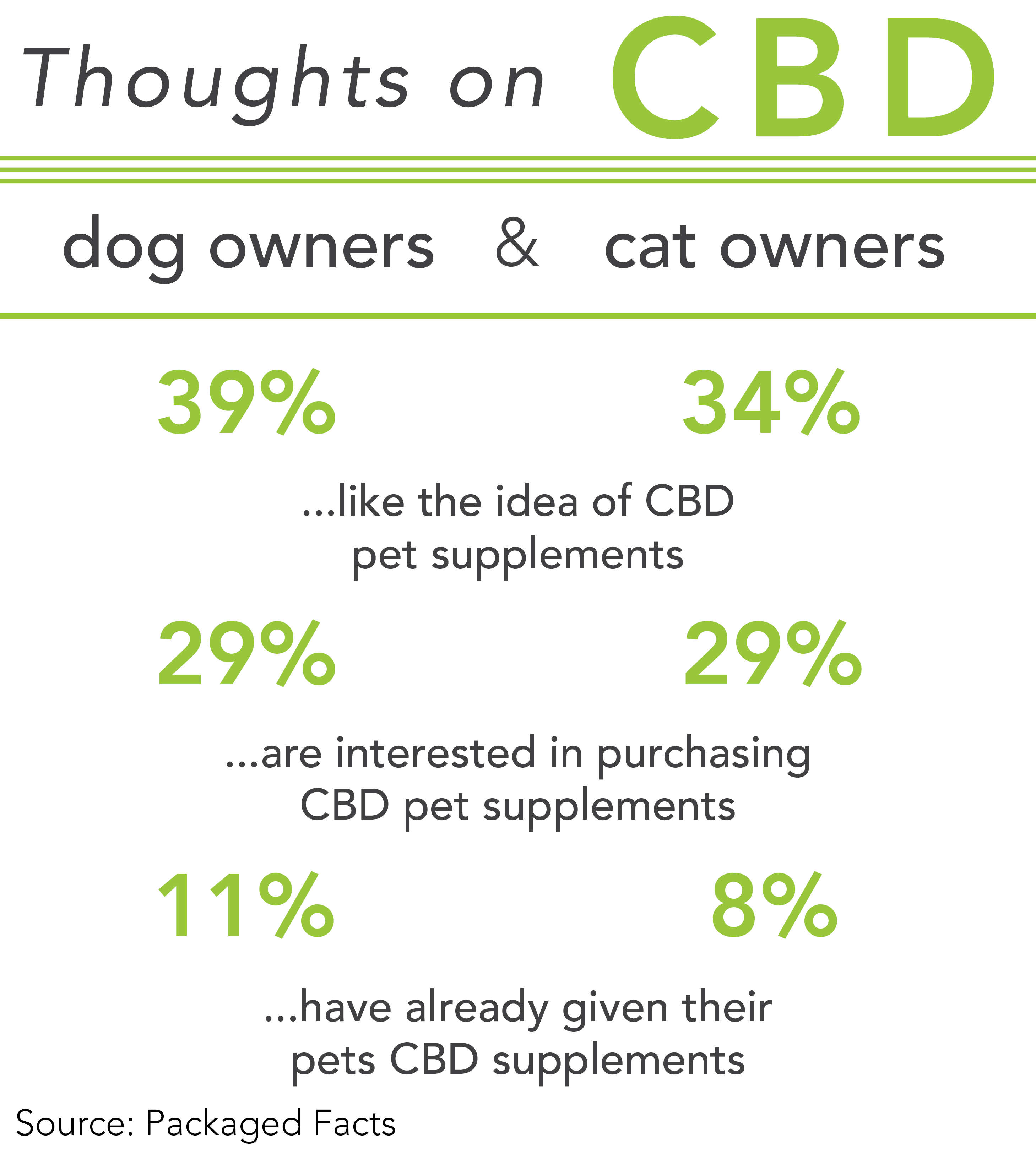

Pet food and treats with functional claims that promise to support joints, skin and coat health, endurance and digestion, just to name a few, are gaining in popularity. Mirroring the human food market, products containing hemp, including cannabidiol (CBD), are exploding and far outpacing the regulatory agencies’ policies on these ingredients – just another area where this industry is breaking the rules.

Pet food and treats with functional claims that promise to support joints, skin and coat health, endurance and digestion, just to name a few, are gaining in popularity. Mirroring the human food market, products containing hemp, including cannabidiol (CBD), are exploding and far outpacing the regulatory agencies’ policies on these ingredients – just another area where this industry is breaking the rules.

As more traditionally premium and super-premium brands take an omnichannel approach, retailers — both traditional and online — are competing with house brands for shelf space or online position. Novel ingredients are grabbing the headlines, processors are learning how to navigate an increasingly complex market, and top brands are steering their products into sales success.

Competing with private label brands for shelf space or online position is just one more obstacle top pet food and treat companies must overcome in the modern market. Fortunately, US pet food manufacturers are in a strong position, owning nearly half of the global market. Processors are learning how to navigate an increasingly complex market and top brands are steering their products into sales success.

|

|

Keep up with the latest pet food trends on our Trends page.