DANIA BEACH, FLA. — In a letter to shareholders, Sumit Singh, chief executive officer, referred to 2020 and 2021 as “the most remarkable two-year period” in Chewy’s history. The company benefitted from retail channel shifts and accelerated trends in the online pet care space, driving a $4 billion or 83% increase in net sales over the last two years, Singh shared. Over that same period, the company increased its active customers by 7.2 million, or 54%.

On March 29, the online pet retail giant shared its fourth-quarter and fiscal 2021 earnings, detailing double-digit net sales growth over both periods.

Source: Chewy, Inc.

Source: Chewy, Inc.

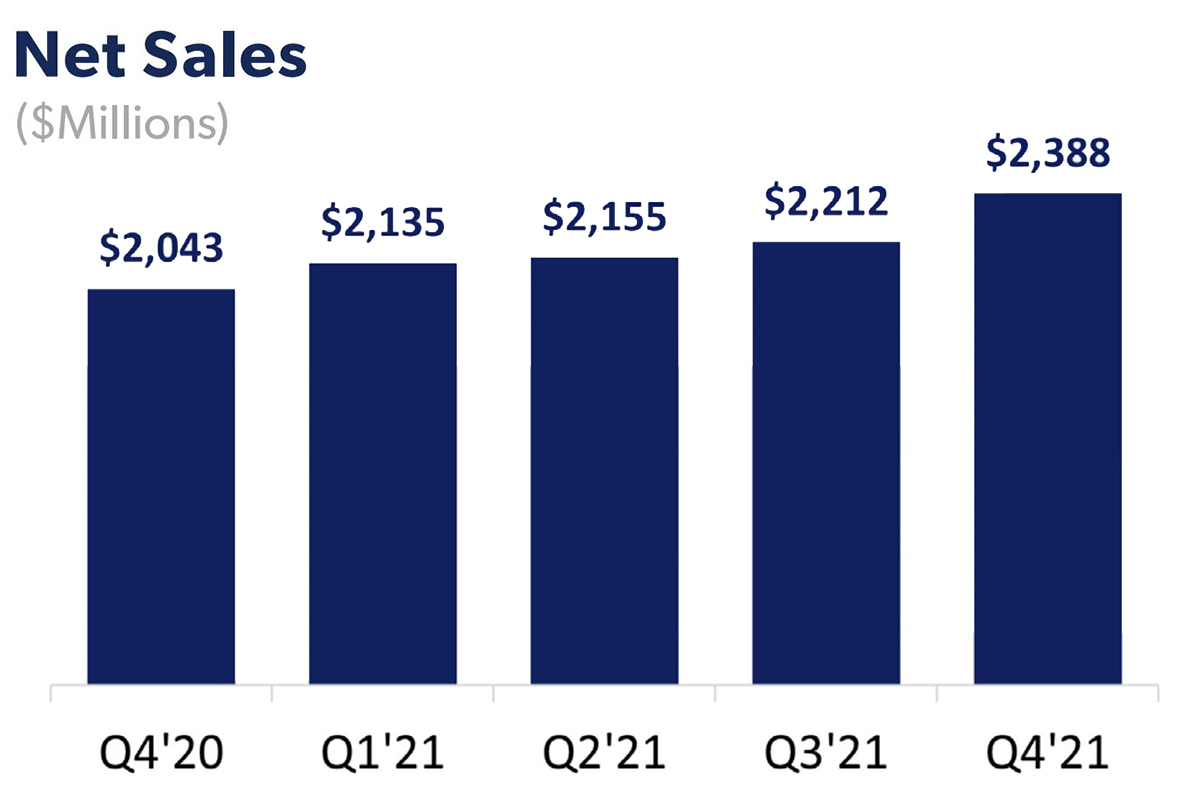

For the fourth quarter ended Jan. 30, 2022, Chewy reported a net loss of $63.6 million, which includes share-based compensation expenses of $15.8 million. Net sales topped $2.39 billion, up 17% from the previous fourth quarter. Adjusted EBITDA, however, was down $88.9 million, or 146.3%, year-over-year to negative $28.1 million.

Chewy’s full fiscal year performance showed a net loss of $73.8 million, including share-based compensation expenses of $85.3 million. Net sales totaled $8.89 billion, up 24% from fiscal 2020, and adjusted EBITDA was $78.6 million, down $6.6 million from fiscal 2020.

“Our ability to deliver 24% net sales growth in 2021, on top of the outsized growth we delivered last year, reflects the durability of our business and the pet category beyond the near-term benefits of the pandemic, and is a strong testament to Chewy’s ability to execute in the face of rapidly evolving macro conditions,” Singh said. “Net sales per active customer, or NSPAC, of $430 is a new company high and demonstrates strong customer loyalty and engagement on our platform, as well as our ability to steadily grow share of wallet. As we look to 2022 and beyond, our innovation pipeline remains robust, our strategy remains intact, and we remain optimistic about the growth opportunity ahead of us.”

Autoship subscription sales continue to be the kingpin for growth at Chewy, Inc. Autoship sales totaled $1.69 million over the fourth quarter, up 21.2% from year-ago sales and representing 70.7% of the pet retailer’s total fourth quarter net sales. In fiscal 2021, autoship sales totaled $6.25 million, up 27.7% from 2020 and accounting for 70.2% of the company’s total net sales.

Source: Chewy, Inc.

Source: Chewy, Inc.

Chewy now has 20.7 million active customers, up 7.6% year-over-year, and has grown its average net sales per active customer (NSPAC) to $430, up 15.6% from 2020.

“As a proof point of the sustainability of NSPAC growth over time, our oldest cohorts are now spending nearly $1,000 per year with us,” Singh said in Chewy’s March 29 earnings call. “While the fourth quarter was the strongest quarter of 2021 for gross customer adds, net adds at 0.3 million were below our expectations.”

Strong demand, however, was coupled with supply chain challenges seen across the industry. Chewy was not spared these challenges.

“What we saw play out in the fourth quarter of 2021 was a tug between the fundamentally strong consumer demand that underpins our business and the highly challenging operating environment,” Singh said.

Cost inflation and increased inbound freight costs caused Chewy’s gross margin to decline 170 basis points in the fourth quarter, coming to 25.4%, while full-year gross margin was up 120 basis points to 26.7%, a “new company high” despite inflated costs and transportation challenges faced in the second half of 2021, Singh shared. Starting January 2022, the company will move on an outbound shipping contract with FedEx, which is expected to increase its gross margins between 100 and 150 basis points over fiscal 2022. Additionally, Singh noted the company is considering several initiatives along its supply chain and logistics operations to lower freight costs moving forward.

“As we close the book on 2021 and move forward in 2022, we are already seeing improvements in labor availability, inbound shipping costs, and pricing, while out-of-stock levels and outbound shipping costs remain elevated,” Singh stated in the shareholder letter.

Mario J. Marte, chief financial officer at Chewy, detailed the company’s capital spending geared toward capacity growth and internal infrastructure over the fourth quarter of fiscal 2021.

“Capital investments in the quarter continued to be growth-oriented and included spending on our recently opened FC [fulfillment center] in Kansas City, our recently opened pharmacy in Pennsylvania, our soon to be opened FC in Reno, and continued investments in IT infrastructure,” Marte said.

Looking to 2022 and beyond, Chewy will focus on three categories: fresh and prepared pet foods, pet healthcare, and new programs for its customers and advertisers.

The retailer hopes to take leadership in fresh and prepared pet food products, a market it expects to exceed $3 billion in sales by 2025. To this end, Chewy has expanded its selection of JustFoodForDogs products, building on its partnership with Freshpet and its own fresh meals under the Tylee’s brand to offer a broader range of fresh meals, toppers and treats.

“We believe this broad assortment, alongside our credibility with customers, ability to offer education through our differentiated customer service and reliable delivery experience through our world-class fulfillment network will position us well to become the #1 destination for fresh and prepared meals,” Singh said.

Chewy Pharmacy saw sales growth of 75% over the fourth quarter, and Chewy Health continues to gain market share, according to Singh. The launch and expansion of Practice Hub is expected to continue to support the retailer’s position as a veterinary marketplace, and the retailer plans to roll out an assortment of preventative pet health programs and pet health insurance plans later this year.

Additionally, Chewy shared it will launch a customer loyalty program in 2023, alongside a Sponsored Ads program to scale contextual advertising capabilities for its suppliers.

Chewy’s fiscal 2022 guidance projects net sales between $10.2 billion and $10.4 billion, which would represent 15% to 17% growth from fiscal 2021, and a breakeven to 1% increase in its adjusted EBITDA margin.

“Each of us is looking beyond the present operating volatility and into the future with the firm belief that the secular trends of higher pet ownership and increasing online pet penetration will long outlast the term disruption that we see today from the pandemic and it's after effects,” Singh concluded. “…As we execute 2022 and plan 2023 and beyond, we are as optimistic as we have ever been on the long-term growth opportunity ahead of us.”

Read more about corporate strategy, financial performance, mergers and acquisitions on our Business page.