KANSAS CITY, MO. — The pet food industry “passed its recession-resistance test with flying colors,” said Jared Koerten, industry manager of food and nutrition at Euromonitor International, during his presentation at the American Feed Industry Association’s (AFIA) 2021 Pet Food Conference, held virtually Jan. 26.

Koerten’s presentation kicked off the event on Tuesday morning, which reflected on a year of challenges but also a year of opportunity, adaptation and positive growth for the global pet food industry. Leading up to 2020, sales in this sector were accelerating rapidly and, even throughout the pandemic, the market’s growth potential remains resilient.

“In fact, 2019 was the strongest growth that we’ve seen in a decade in the industry, so the market had a lot of momentum as we talk about where we were coming into the pandemic in 2020,” Koerten said.

The global pet care market sales reached $125 billion in 2019, reflecting more than 6% growth from 2018. Dog and cat food sales makes up roughly 70% of the total global pet care revenue and represents a continued non-discretionary investment from pet owners, making it a strong sub-segment of this sector despite COVID-19.

Global pet food sales have been growing over the last decade both in volume and price point, Koerten explained, due to widespread pet humanization and product premiumization.

“If we just look at the average unit price for global pet food over the past decade, we can see that’s risen by nearly 35%, which significantly outpaces general price growth and inflation over that span,” Koerten said.

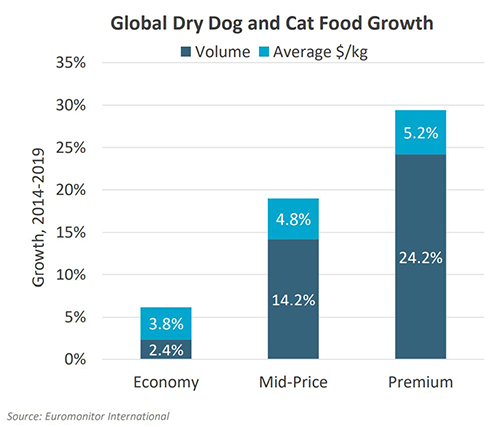

When split into three price-points — economy, mid-price and premium — high-end pet food products still reap the highest improvements, growing 5.2% in average price per kilogram and 24.2% in volume between 2014 and 2019. This indicates more and more pet owners are trading up to higher-quality, higher-priced products.

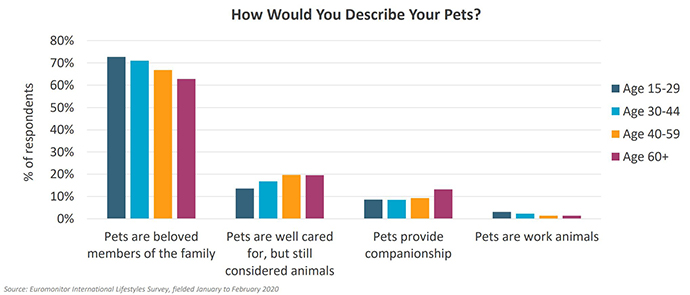

This trend is only expected to grow as younger generations become pet owners and claim their power of setting influential market trends. In a Euromonitor study including 23,000 consumers across 40 global markets, more than 70% of respondents categorized pets as “beloved members of the family.” This humanization of pets is seen more widely in pet owners between the ages of 15 and 44.

“There’s a clear pattern in that younger generations are much more aligned and have bought in to this pet humanization trend more than any other generation,” Koerten said. “So, as we think about the future and as that next group of pet owners comes into the market — as they become the majority of pet owners worldwide — we can see the future is very bright because they already are very much on-board with this pet humanization trend that has been driving the market historically.”

Koerten touched on four key industry challenges that impacted the market in 2020, some of which are expected to continue shaping the market going forward. These included the global economic outlook, supply chain issues, channel shifts and a rise in pet ownership.

The macroenvironment

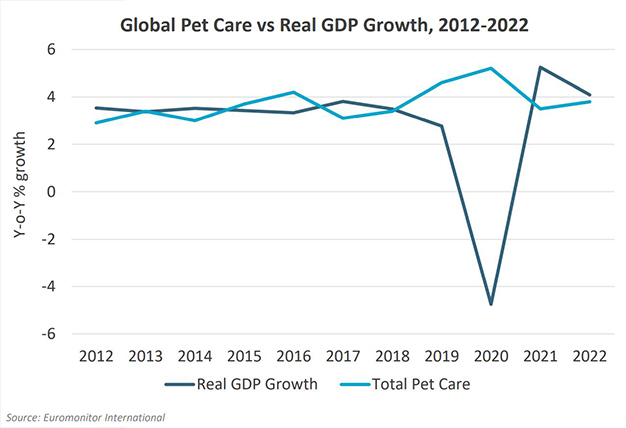

Looking at the macroenvironment, Koerten shared real global GDP data that provided a bleak snapshot of the 2020 global economy.

“This is by far one of the most severe downturns that probably many of us has seen in our lifetimes,” he said, referring to a real global GDP drop of more than 4% from 2019 to 2020.

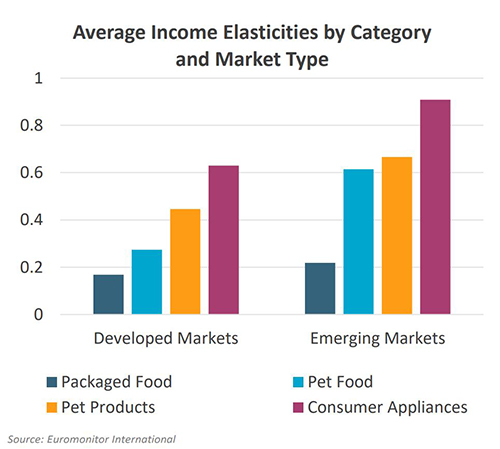

Some sectors such as consumer appliances, personal accessories, luxury goods and apparel were hit hard by this economic downturn, as consumers found themselves with less discretionary income. However, the income inelasticity — or how responsive consumer spending is to changes in income — of the pet food category tells a different story.

“In developed markets, we can see the income elasticity for pet food is very, very low,” he said. “In fact, it’s really close to packaged food, which is probably the lowest you’ll find because people have to eat even in the midst of a recession.

“In emerging markets, it’s a slightly different story. You don’t necessarily have that cushion that you have in developed markets so pet food [spending] is a bit more responsive, but it’s still much, much better than a situation in the durables industry, like consumer appliances.”

Supply chain challenges

Early in 2020, most of the world was caught off-guard and ill-prepared for the pandemic. Employee absenteeism and the mitigation of essential worker safety impacted supplier mobility and led to an overall slowing of global trade traffic between and within most countries.

“In markets like France, the US or China, which are very export-driven and tend to export a lot more than they import, this could be a potential obstacle and could create some headaches moving forward as, again, I think it’s going to be several years before we see overall global traffic get back to where it was in terms of people moving across borders,” Koerten said.

In countries that rely more on imports than exports, such as the United Kingdom, Japan and Italy, these impacts could create continued shortages of certain goods.

Koerten explained that there are two factors that affected the global supply chain in 2020: price and scale. Rising costs and inflationary pressures for commodities, high demand and constrained supply of personal protective equipment (PPE), and fluctuations in the workforce were all obstacles on the price front.

In terms of scale, Koerten said, “Bigger companies that have larger supply chains and more distributors and more options to source from have a bit easier time adjusting than, say, a very small company that relies on a single manufacturer or single distributor.”

Accelerated channel shifts

As we all know by now, social distancing and public health concerns resulted in a surge in e-commerce for several sectors, the pet care industry included. But Koerten emphasized that this trend was already graining traction and was only accelerated by the pandemic.

“E-commerce had been gaining a lot of share, really at the expense of all store-based retailers. But in 2021, that jump is very, very profound here in terms of that share,” he said. “…E-commerce has really become the only option in some cases who are, again, looking to distance as much as possible.”

Consumer mobility data gathered through Google showed that traffic to retail and recreation locations in 2020 dropped more than 60% in March and has been slowly climbing back up since, but still remains significantly lower than pre-pandemic foot traffic.

Countries’ abilities to adapt to this e-commerce surge relied largely on their preexisting infrastructure for that channel, Koerten said.

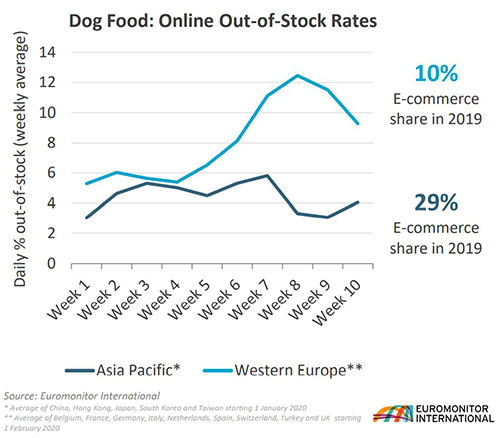

“Before the pandemic, the average out-of-stock rate [for major online retailers in western Europe] was around 5%, pretty standard when you look across markets. Once the pandemic hit though, in late March and into early April, that surged. The out-of-stock rate nearly tripled as everybody went online during quarantines and lockdowns trying to find product during that time… In the UK by early April, nearly one in four dog food SKUs online were out-of-stock during that time.”

He went on to explain that nearly 30% of all pet care sales across Asia in 2019 were made through e-commerce platforms, with an even higher share of more than 50% in South Korea and China. In western Europe during the same time frame, e-commerce accounted for only 10% of total pet care sales. Because of the infrastructure already built out in Asia to handle online demand for pet products, markets in that region did not experience the same increases in out-of-stock rates as western European retailers.

He went on to explain that nearly 30% of all pet care sales across Asia in 2019 were made through e-commerce platforms, with an even higher share of more than 50% in South Korea and China. In western Europe during the same time frame, e-commerce accounted for only 10% of total pet care sales. Because of the infrastructure already built out in Asia to handle online demand for pet products, markets in that region did not experience the same increases in out-of-stock rates as western European retailers.

This trend toward e-commerce is what Koerten called “sticky,” meaning after gaining channel share during the pandemic, it’s not likely to taper off post-pandemic. The convenience offered by subscription-based e-commerce purchases, curbside delivery, third-party delivery and direct-to-consumer models is likely to continue stealing share from more traditional brick-and-mortar outlets.

“Nearly 70% of Chewy sales come from its set-and-forget auto-ship customers, who are very likely to remain in that model moving forward,” Koerten said. “For Zooplus, 50% of their sales now come from SaverPlan Customers, who are really locked in. They pay the membership fee to get future discounts at Zooplus, so they’re likely to go back there in the future.”

Pet ownership surge

Finally, growing pet ownership rates worldwide are expected to result in increased and continued pet food purchases. Koerten said more businesses are likely to adapt remote working to the long-term, providing employees more flexible hours, work-from-home options and maybe even letting pets into the workspace more often.

“I think the industry passed its recession-resistance test with flying colors. Overall, the positive drivers that we’ve talked about — the new adoptions, the bonding, the higher prices, the higher costs — more than outweigh the income effects of that low income elasticity, and… even though real GDP growth plummeted here in 2020, our pet care industry has seen its strongest year we have, at least on our historic records.”

“I think the industry passed its recession-resistance test with flying colors. Overall, the positive drivers that we’ve talked about — the new adoptions, the bonding, the higher prices, the higher costs — more than outweigh the income effects of that low income elasticity, and… even though real GDP growth plummeted here in 2020, our pet care industry has seen its strongest year we have, at least on our historic records.”

As we look forward in this industry, Koerten pointed to three trends to look for as the industry continues to evolve: automation in the retail space, more purpose-driven shopping experiences, and new ways for brands to engage with consumers digitally. All these trends are a direct result of social distancing practices perpetuated during the COVID-19 pandemic, which continues to impact the global economy and the way consumers shop.

Keep up with the latest pet food trends on our Trends page.