KANSAS CITY, MO. — As economic repercussions of the coronavirus pandemic persist in the United States, pet food processors have expressed a variation of impacts, opportunities and expectations for their workforces, supply chains, retail sales and production over the last three months and well into the future.

Pet Food Processing conducted a follow-up survey to its previous COVID-19 impact questionnaire to gauge long-term sentiments of pet food and treat manufacturers on market volatility, economic hardship and lasting changes to improve worker safety and sanitation. Below are some shared and individual responses collected through our follow-up survey.

Summary

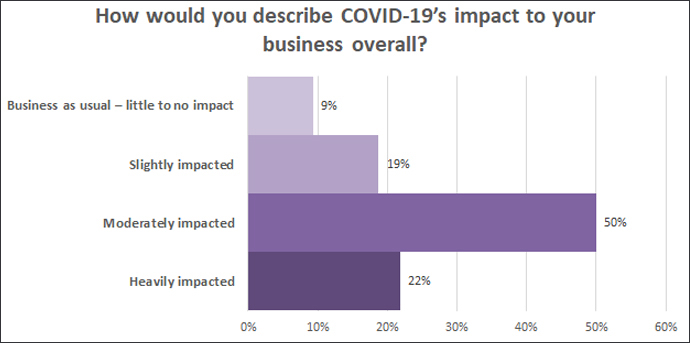

The overall impact of COVID-19 to most pet food companies has seemed to taper off since the pandemic first hit the United States in March. Half of respondents reported their businesses have been moderately impacted by the public health crisis, while 22% said they have been heavily impacted and 19% said they have been only slightly impacted. The other 9% of respondents said they have assumed business as usual throughout the pandemic.

Although the initial surge in demand caused by consumers stocking up on non-discretionary household items — such as pet food — seems to have ended in late April, many respondents (44%) reported their business has seen an overall increase in production compared to the same time last year. On the flip side, compared to a year ago, 22% of respondents have seen production substantially down and 12% reported production is slightly down, while 16% have seen little to no impact. The remaining 6% of respondents reported a "wide fluctuation in demand," but close to normal production compared to year-ago numbers.

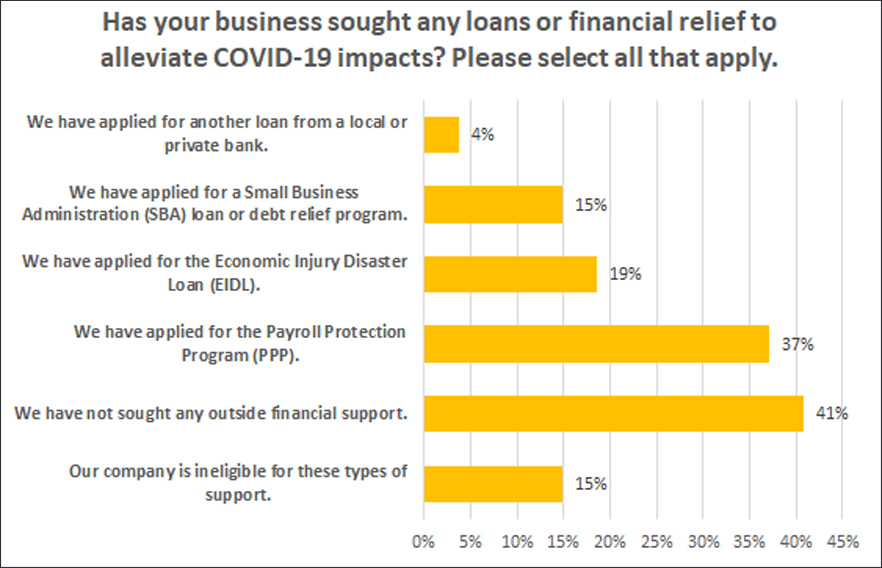

When asked if their business had sought any financial assistance during the pandemic, 37% of respondents said they had applied for the Payroll Protection Program loan (PPP), 18% said they had applied for the Economic Injury Disaster Loan (EIDL), and 14% said they had applied for a Small Business Administration (SBA) loan or debt relief program. A majority (40%) of respondents said they had not sought financial support, 15% said their company is ineligible for these aid programs, and 4% said they had applied for a loan from a private or local bank.

Of those who applied for a PPP loan, 40% of respondents said they have since received the aid. This goes for 18% of those who applied for the EIDL loan, 14% of those who applied for an SBA loan or debt relief program, and 5% who said they applied for a local or private bank loan.

Most respondents (53%) reported they are operating with a normal-sized workforce, but 34% of respondents said they are understaffed due to employee illness or other direct impacts of COVID-19. Another 9% said they are operating with a smaller workforce due to decreased demand for their product, while 3% reported they are operating with a larger-than-normal workforce due to increased demand.

A majority of respondents (81%) said they have not had to stop production for any period of time as a result of the pandemic. The 19% respondents that did shut down temporarily cited labor shortages due to employee concerns, shutting down to give employees the opportunity to quarantine, or waiting for loan assistance.

More than one quarter of respondents (26%) said while they continue to distribute product outside of the United States, their business abroad has not been impacted by COVID-19. One manufacturer reported its business in Japan has been impacted by the pandemic, with another reported increased freight costs and lead times. Another processor explained foreign exchange rates are beginning to "have an adverse effect" on their business overseas.

Retail trends

Retail trends

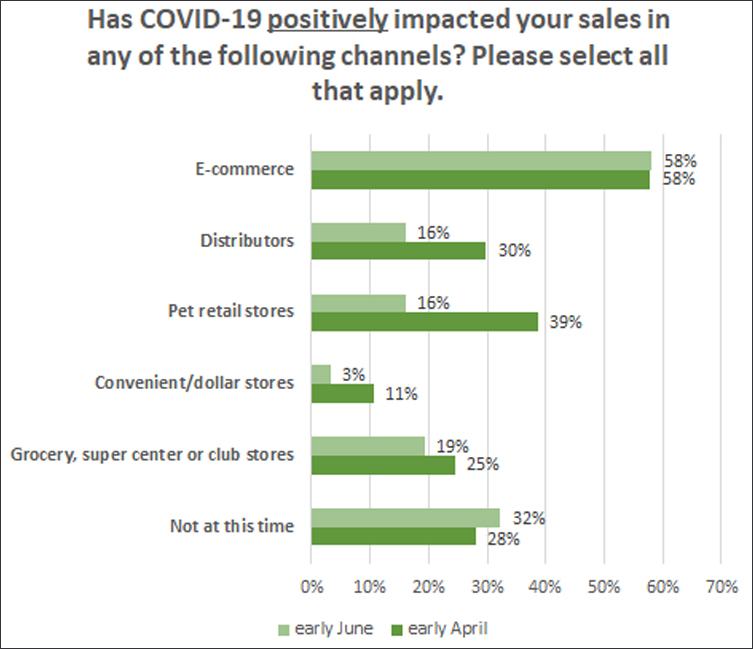

Increased e-commerce sales were reported by 58% of respondents between March and May, while 19% said sales in the mass market have been positively affected as well. Approximately 16% respondents said both pet retail and distributor sales are up, while just 3% reported increased sales in convenient and dollar stores. Thirty-two percent of respondents said sales have not been impacted in any of these channels.

This represents a steadfast positive impact in e-commerce sales compared to our previous COVID-19 impact survey, in which 57% of those surveyed reported increased sales in that channel.

In contrast, positive sales impacts in the distributor, pet specialty retail, mass market and convenient/dollar store channels seem to have deflated between early April and early June, with fewer respondents reporting increased sales in these retail spaces.

The gradual shift from brick-and-mortar pet retail to e-commerce is only being exacerbated by the COVID-19 situation, with one pet retailer citing short-term declines in retail sales that they expect to see continue in the long-term, as well as an anticipated short-term cost of approximately $85,000 due to COVID-19 impacts.

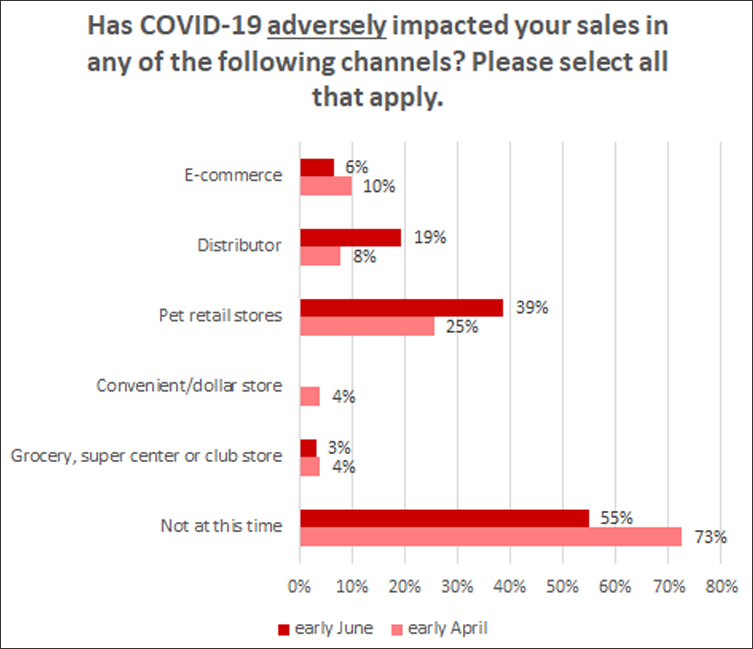

In terms of negative impacts across these sales channels, the majority of respondents (55%) reported sales have not been negatively impacted by COVID-19 between March and May. Pet specialty retail sales, on the other hand, were down for 39% of respondents, and distributor sales remain down for 19%.

This reflects a continued decline in pet specialty and distributor sales when compared with our previous survey, in which just 25% of respondents reported pet specialty sales were down and 7% of respondents said distributor sales had been negatively impacted.

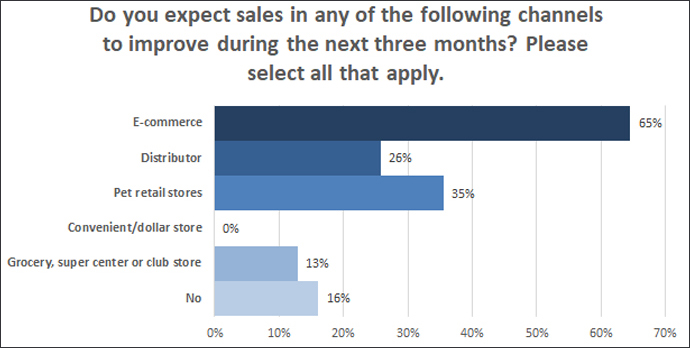

Over the next three months (through mid-August), 64.5% of respondents said they expect e-commerce sales to improve, 35.5% said they expect pet specialty sales to improve, and 25.8% expect distributor sales to improve.

Additionally, nearly 26% of respondents said they have added e-commerce capabilities amid the pandemic, either through a third-party platform (13%) or their own online store (13%).

Growing supply chain challenges

Supply chain issues among direct-to-consumer and e-commerce platforms were also reported.

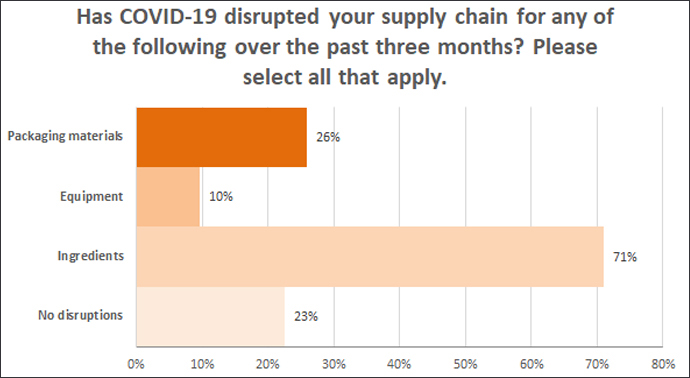

Supply chains for pet food and treat processors seem to remain in a state of flux. Half (50%) of respondents said they had not experienced supply chain disruptions in late March, compared to just 22.6% of respondents reporting no disruptions over the last three months. Seventy-one percent said they have seen disruptions along their ingredient supply chains over the last three months, compared to just 43% in late March.

Additionally, 25.8% reported disruptions for packaging materials over the last three months, compared to just 17% previously, and 9.7% said their equipment supply chains have been impacted compared to 5% of respondents in late March.

Slightly over half (53%) of survey respondents reported no disruptions to product distribution over the last three months, with the other 47% reporting disruptions as some distributors seem to be operating with caution.

Continuing with caution

Companies are continuing to implement new policies to protect employee health and safety, such as increased sanitation measures, enforcing social distancing and mandatory PPE, allowing eligible employees to work from home, monitoring employee health through temperature checks, limiting facility access and restricting travel.

Most respondents (67%) said they are allowing eligible employees to continue working from home, with 10% providing the option to work from home or in the office, and 23% reporting all personnel are back working on-site.

Almost all respondents (93.6%) reported limited manufacturing facility access to only essential personnel. Nearly 80% said they are still restricting employee travel by either ceasing it entirely or allowing it only under special circumstances.

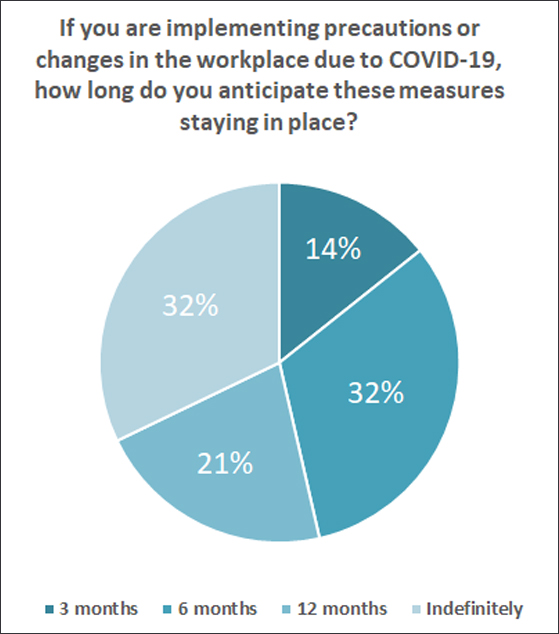

The majority of those surveyed who have implemented safety and health policies during the pandemic said they expect those procedures to be in place for at least 6 months, with 21% planning to continue them for another 12 months, and 32% expecting to adopt them indefinitely.

What the future holds

Most processors (38%) anticipate increased demand to persist over the next three months (through mid-August), while 28% are bracing for continued market volatility and fluctuating demand.

Processors expressed a myriad of concerns they expect to face over the next three to six months, including mitigating the risk of employee illnesses and staffing challenges, fluctuating demand and economic confidence or buying power among consumers, increased e-commerce competition, a slow recovery for brick-and-mortar pet retail, uncertain ingredient supplies and price fluctuations, and the potential of facility closures if the virus continues to spread across the United States.

Stay informed about how the coronavirus pandemic is affecting pet food and treat processors by visiting our COVID-19 topic page.

For more context, read a summary of our previous COVID-19 survey, in which pet food processors shared initial impacts of the pandemic.

Pet Food Processing's COVID-19 Impact Follow-Up Survey was fielded from May 28 to June 3. A majority of respondents classified themselves as pet food or treat manufacturers (72%), 16% were pet food and treat suppliers, 6% were product distributors, 3% were pet retailers, and the remaining 3% are wholesale feed manufacturers.