This article was published in Pet Food Processing's 2019 Resource Guide. Read it and other articles from this issue in our Resource Guide digital edition.

The market shift to super premium pet food and treats is forcing processors to pivot and adapt production. Processors hope to chase trends with a conservative approach to capital expenditure until it’s clear the trend they are chasing is here to stay. But 2019 served up some curveballs as quality grains gained prominence in new product offerings and grain-free took a hit from the US Food and Drug Administration’s (FDA) inquiry into canine dilated cardiomyopathy (DCM). It’s a challenge to confidently commit capital dollars toward a niche product when, to borrow a phrase from Heidi Klum, “One day you are in, the next you are out.”

Overall, processors expressed excitement for the opportunities they see in the industry. Expanded distribution into new sales channels, continued market growth and a shift to premium products are contributing to the positive outlook for this year. While 100% of industry executives surveyed reported an overall positive outlook for pet treats, the outlook for pet food was still nothing to bark at with 96% of executives giving it a thumbs up.

30% of executives surveyed expect to add a new production line within the year.

The challenges threatening to cloud the skies in 2020 were reported to be the lack of a skilled workforce (47%), food safety (39%) and rapidly changing consumer attitudes (35%).

The survey reached out to US pet food and treat companies that either manufacture products in company-owned processing facilities (71%), co-manufacture for other companies (43%), utilize other manufacturers to process products (32%), or some combination of these three. The companies reported an average of 84% of revenue coming from North American sales.

Riding high

While 70% reported an increase in company revenue in 2018 compared to 2017, even more (78%) expect their company’s revenue to be higher in 2019 compared to 2018. That represents a 15.6% increase from 2018 to 2019. The growth is predicted to come from several areas including existing product lines in the US (63%), new product launches (61%), new distribution channels (53%), growth of existing product lines in international markets (29%), and by offering additional packaging formats (27%).

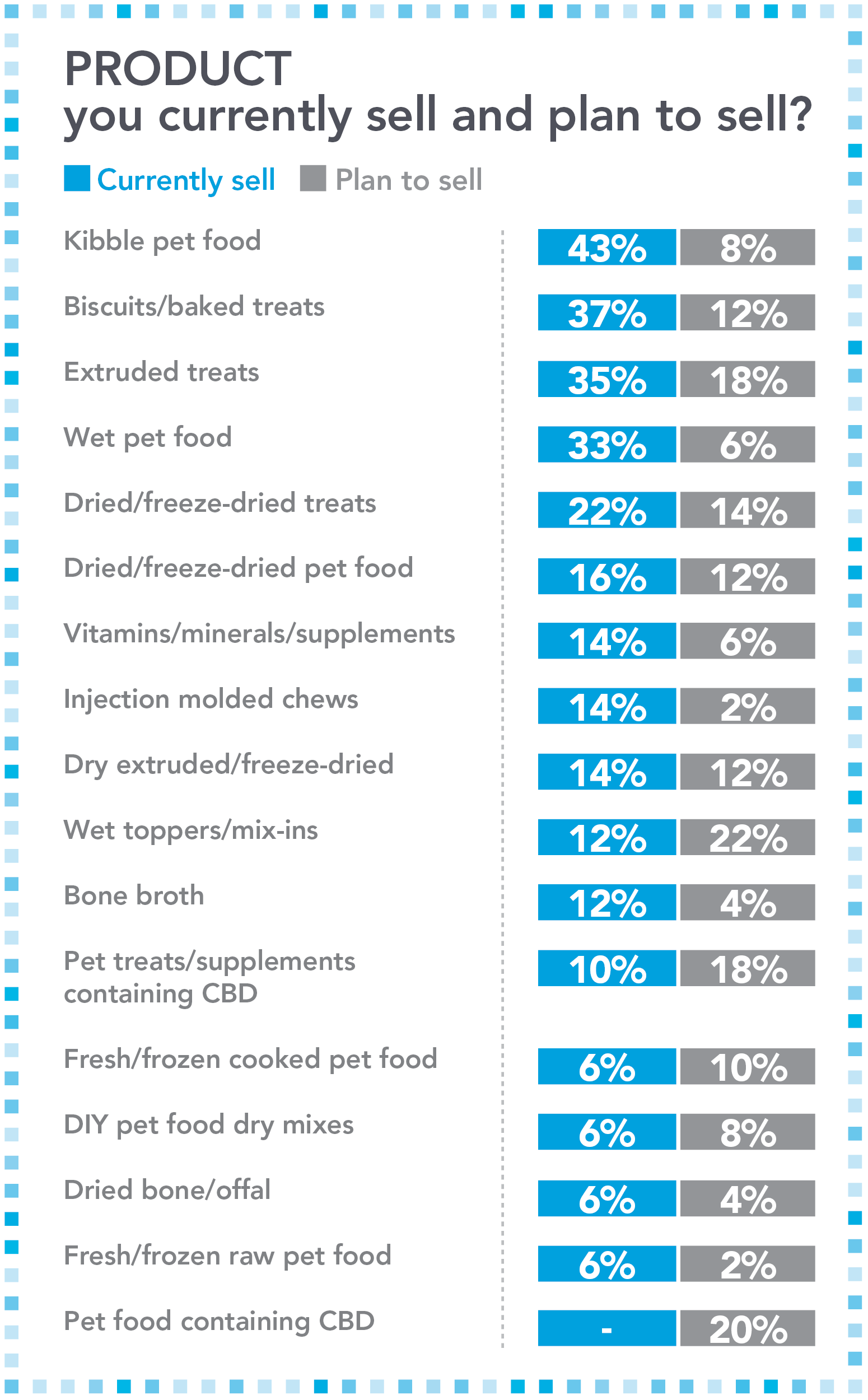

Current product offerings of the surveyed companies include kibble (43%), biscuits and baked treats (37%), extruded treats (35%) and wet pet food (33%). The new product launches expected to deliver growth over the next two years include wet toppers and mix-ins (22%) and pet food containing CBD (20%). Extruded treats (18%) and pet treats or supplements containing CBD (18%) were also high on that list.

In this omni-channel era of meeting customers where they shop, survey respondents confirmed the use of a multi-channel distribution approach. A majority of respondents (66%) sell through independent pet specialty retailers, 50% reported distribution through national pet retail chains, 46% through major e-commerce retailers, 36% through Food, Drug and Mass (FDM) channel retailers and 30% through company-owned e-commerce channels. The companies surveyed were asked to identify all of the relevant distribution channels through which their company currently markets products.

With 76% reporting some revenue from e-commerce, that channel accounted for an average of 14% of the responding companies’ current revenues. For 10% of the companies, e-commerce sales represent 31% or more of their annual revenues.

Strategic spending

As consumers continue to vote for brands with their purchasing dollars, a wider variety of food and treat formats are gaining traction. Consumer pet spending was up 25% from $58 billion in 2014 to more than $72 billion in 2018, according to the American Pet Products Association (APPA) National Pet Owners Survey, 2019-2020. Pet food sales accounted for 41.8% of the US pet industry’s total revenue in 2018, and APPA projects they will continue to grow 4.5% to a total of $31.68 billion by the end of 2019.

Although dry kibble still dominates the US pet food market with 72% of sales, the increased focus on pet wellness has pet owners feeding a broader range of products to their pets, according to consumer goods market research firm Packaged Facts. Producing a wider array of products presents manufacturing challenges and requires capital investment. The majority of executives (65%) reported an increase in capital spending for 2019 versus 2018 and 51% expect increased capital investments during the next two years.

61% of respondents plan to launch new products to drive growth.

What goals are driving capital investment? Improving processing capability and flexibility was reported as the top capital spending goal. Also important is improving food safety and sanitation, as well as increasing capacity for existing products. To achieve these goals, the majority of companies plan to allocate dollars for maintenance and replacement parts (61%) and system improvements (61%). Another priority is purchasing new processing equipment (43%).

Nearly one third of respondents (30%) plan to add a new production line within the year. Major expansions of existing facilities are on tap for 24% of companies and a few (17%) have plans for a new facility, either through construction or purchasing an existing structure.

The other side of the coin

The continued growth of the US pet food market is good news for industry processors, but a more competitive retail landscape has accompanied that growth. Other market factors are presenting challenges as well. Among them are the availability and cost of skilled labor, the rapidly changing trends and the ever-present food safety concerns.

Encouraging a conservative approach to capital investment is the generally accepted belief that the US pet food market has matured plus the growth of the volume of pet food sold has slowed. When looking outside the US borders for growth, trade relations can be a cause for concern. But, despite reasons to be cautious, this survey indicates a healthy amount of capital investment is still on the table over the next two years.

The demands of this market are keeping processors on their toes, chasing the holy grail of revenue growth and making strategic investments that only time will tell if they were worth it. Processors probably don’t have to wait as long as they did in the past to know which decisions are the right ones. As trends emerge more rapidly and speed-to-market may dictate success or failure, the ability to quickly adapt has become the target. This industry draws people and companies passionate about companion animal nutrition and health. It’s exciting to be part of a “hot” industry and that enthusiasm was reflected in the responses the processors provided, with one classifying the US pet food and treat industry as an “amazing opportunity.”

2019 processor survey sample

For Pet Food Processing’s first ever industry study, Kansas City, Missouri-based Cypress Research Associates, LLC, surveyed upper and mid-level management executives at pet food and treat manufacturers from across the country. The majority of respondents (55%) reported their area of responsibility as corporate management, marketing or sales. Quality control and sanitation accounted for 18% along with R&D and product development. The remaining 27% was evenly distributed across plant operations and production, engineering and maintenance, nutrition, procurement, warehousing and distribution.

Of the survey sample, most companies (59%) produce dog treats and 55% produce dog food. Cat food came in at 41% followed by cat treats at 25%. The next largest participant categories included pet supplements (20%) followed by ingredients (11%). Others included small mammal (9%), reptile (7%) and aquatic (5%). Companies could identify with more than one of these categories.

Additionally, 30% of respondents indicated a company-wide annual gross revenue of $100 million or more, and 18% indicated revenue of less than $1 million. Processors with a gross revenue between $1 million and $19 million represented 20% of the samples, and those between $20 million and $99 million accounted for 22%. Forty-five percent of respondents reported having two or more processing facilities.

Of the companies surveyed, 63% are subject to FDA inspections, 54% to State Department of Agrigulture inspections and 43% to USDA inspections. The online survey was fielded in May and June 2019 and includes results from Pet Food Processing readers.

Read more about pet food processing operations on our Operations page.